The Most Powerful Platform for Options Strategy Backtesting

Explore Historical Returns of Popular Options Strategies and Improve Your Trading

* For informational purposes only. Not financial advice. Data may be delayed or inaccurate.Terms of Use

Platform at a glance

Why Backtest?

Make data-driven decisions based on historical volatility patterns instead of gut feelings

Search for optimal strikes, expirations, and rules that maximize returns and minimize risk

Study past volatility returns around events like earnings to optimize your bet

Distinguish between luck and alpha by running the strategy over many years of data

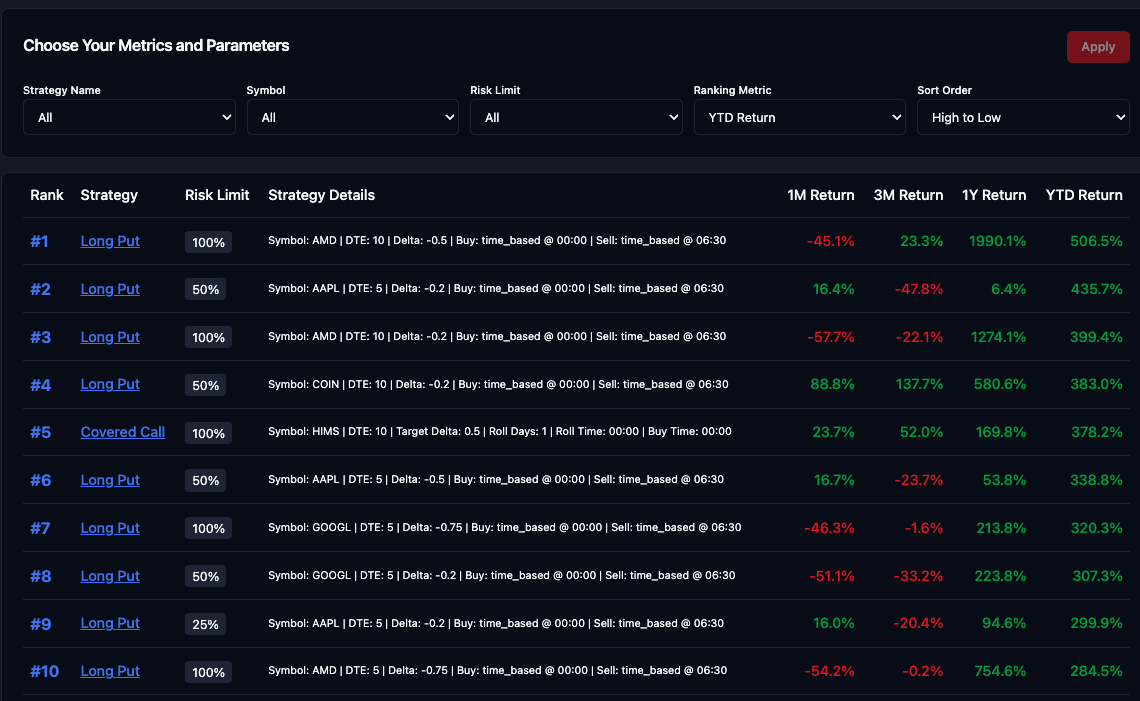

Strategy Leaderboard

Find the strategy with the highest return across symbols and strategies daily. Current strategies include long calls, puts, straddles and covered calls.

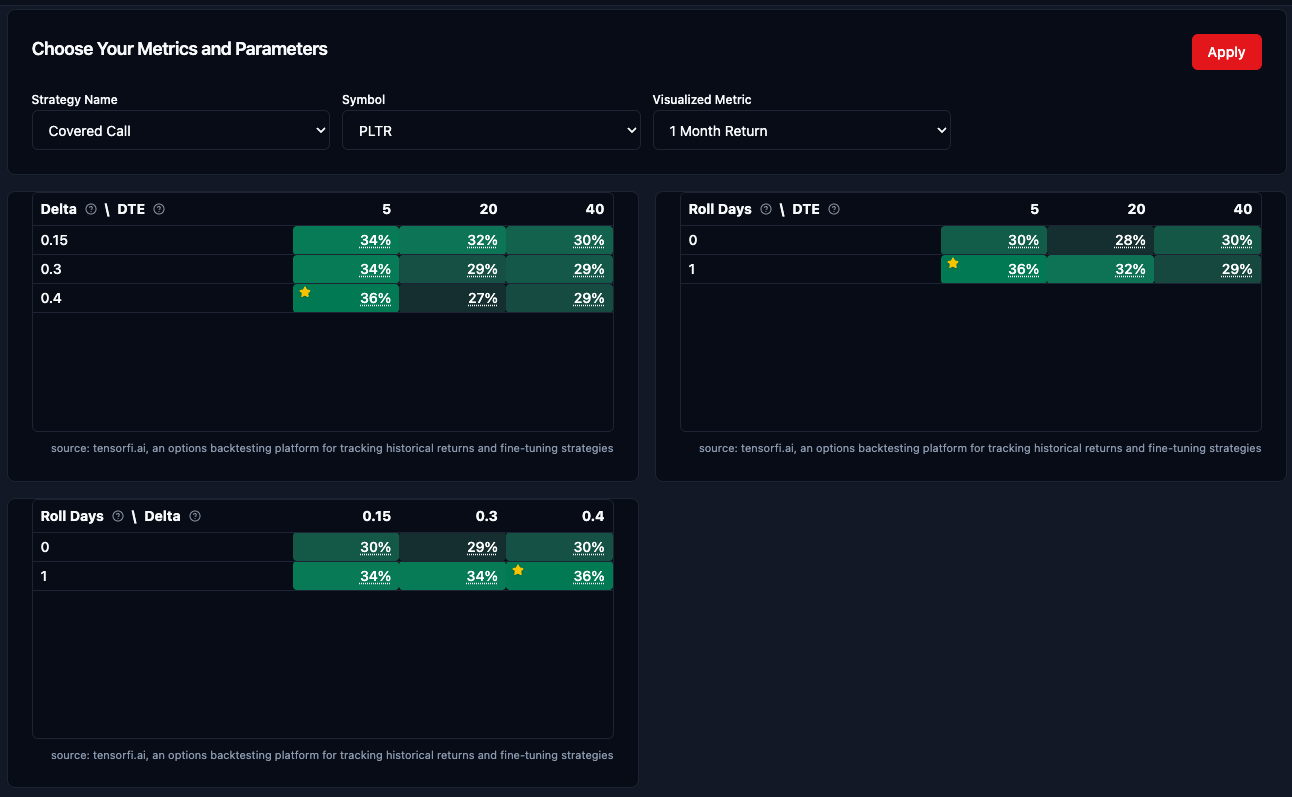

Parameter Visualizer

Visualize how different parameteres affect the return of a chosen strategy. Useful if you are unsure which option delta or expiry to trade.

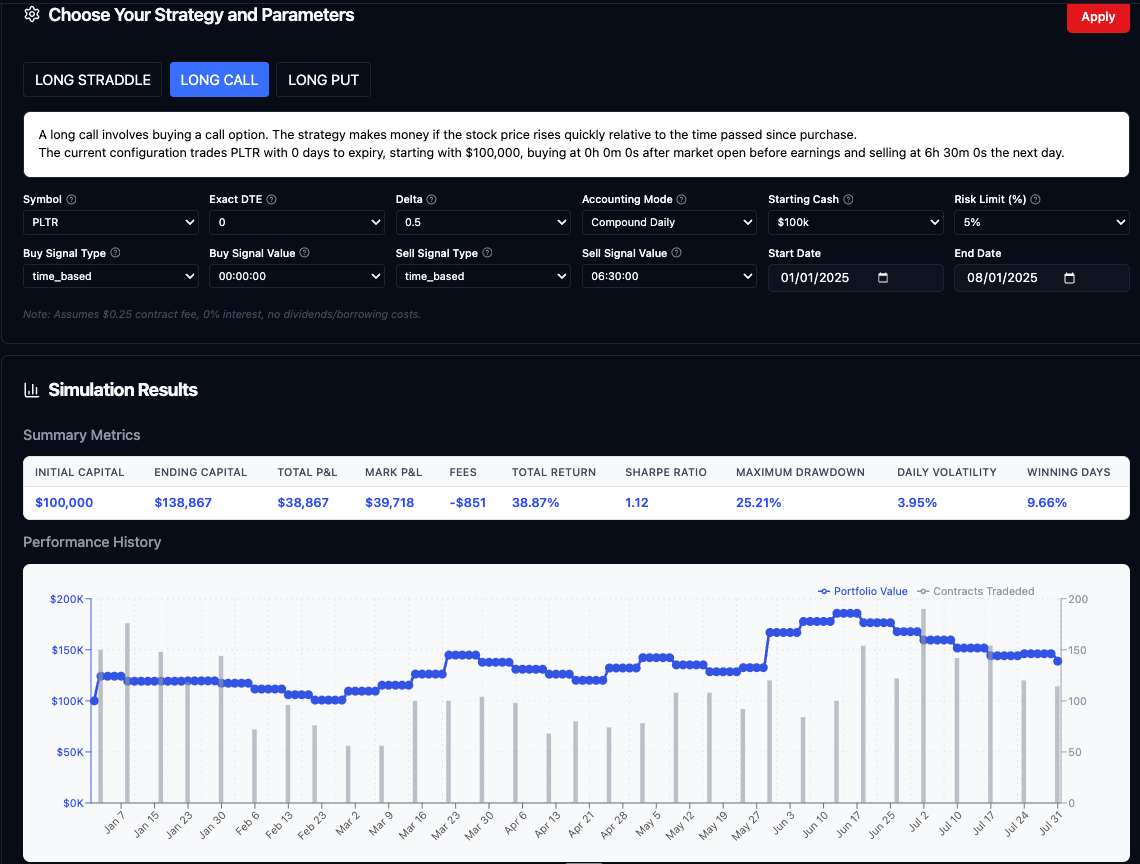

Strategy Drilldown

Examine the detailed daily return and trades for the chosen strategy displayed in a time series. Strategies are grouped into three categories below:

Income-generating strategies that profit from time decay. Trade covered calls and other theta-positive strategies for consistent returns.

Overnight strategies that capitalize on earnings volatility. Buy options before announcements and profit from surprise moves.

Long options strategies like buying calls, puts, and straddles commonly seen on WSB. High risk, high reward.

Frequently Asked Questions

How is backtesting different from paper trading?

Backtesting allows rapid testing of retail strategies in a scalable way - thousands of symbols, strategies and parameters can be tested over years of historical data. Paper trading, by contrast, plays out in real time and is best for confirming live execution on your broker before trading in production.

Does backtesting suffer from hindsight or survivorship bias?

This is certainly a concern and you never want to overfit your strategy. Fundamentally this boils down to whether you think the past is a good predictor of the future for your strategy. Unlike stock returns, options volatility tends to follow more statistical patterns (e.g. mean reversion), so options backtests tend to have more significance.